Watch out! These Filipino movies will inspire you to travel the #PhilippinesFirst.

Tonik Digital Bank in 2026: Is This Digital Bank Still Worth It?

Digital banking has become part of everyday life for many Filipinos, and by 2026, having at least one digital bank account is no longer a novelty. Among the early players in the space is Tonik Digital Bank, which launched in 2021 as the Philippines’ first neobank and has since grown into a familiar name in the local digital finance scene.

So in 2026, with more digital banks available and competition getting tighter, is Tonik Digital Bank still worth using?

Tonik Digital Bank: Services and features

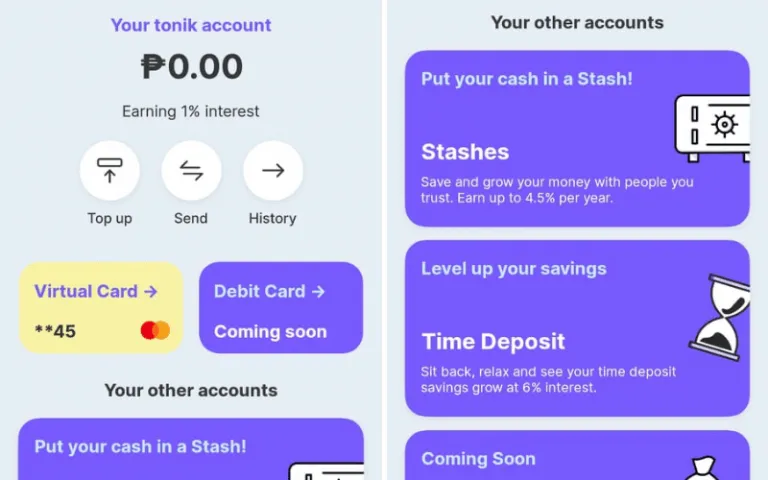

Basically, Tonik operates just like the traditional bank, only it relies solely on technology. It allows deposits, withdrawals, loans, payment, and even card products. Aside from the main account (1% interest p.a.), Tonik offers its users up to five stashes and five time deposit accounts.

What are stashes?

Stashes are digital wallets inside your Tonik account designed to help you save for specific goals. In 2026, Tonik still offers both Solo Stashing and Group Stashing, each typically earning higher interest than a regular savings account, subject to current terms and promotions.

Solo Stashing works well for personal goals such as building an emergency fund, saving for travel, or setting money aside for big purchases. Group Stashing allows users to save together with friends or family toward a shared goal, which can be useful for trips, celebrations, or joint expenses.

How does the Tonik time deposit work?

Time deposits remain one of Tonik’s most attractive features in 2026. Users can open time deposit accounts with competitive interest rates that may go up to 6 percent per annum, depending on the chosen term and ongoing promos.

There is no minimum deposit required, making this feature accessible even for first-time savers. Available terms usually range from six months to two years, allowing users to lock in funds based on their savings timeline.

How does the debit card work?

Every Tonik account comes with a free virtual debit card that can be used for online shopping, subscriptions, and bill payments. Users may also request a physical Mastercard for a one-time fee.

The physical card can be used for ATM withdrawals locally and overseas, with fees depending on the ATM provider rather than Tonik itself.

Also read: Here’s Why We Should Shift Towards Cashless Payments

How safe is the Digital Bank?

Security remains a top concern for digital bank users. Tonik is regulated by the Bangko Sentral ng Pilipinas, and deposits are insured by the Philippine Deposit Insurance Corporation for up to ₱500,000 per depositor.

These protections mean that Tonik operates under the same regulatory framework as traditional banks, offering users added peace of mind when saving digitally.

Is Tonik Digital Bank still worth it in 2026?

For users looking for structured savings tools, competitive interest rates, and a fully app-based banking experience, Tonik remains a solid option in 2026. Its stash and time deposit features continue to stand out, especially for those saving toward specific goals.

That said, as with any digital bank, it works best as part of a broader financial setup. Many users keep Tonik alongside traditional banks or other digital banks, depending on their needs.

Ultimately, whether Tonik is worth it in 2026 depends on how you plan to use it. If high interest savings, goal based features, and convenience matter to you, Tonik still holds its place in the growing digital banking space.

Published at

About Author

Danielle Uy

If Disney were creative enough to let Mulan and Melody procreate, Danielle would be that child. From an early age, she has dreamt of becoming a purposeful revolutionary... and an unruly mermaid. While Danielle hasn't held a sword in her lifetime, she feels powerful enough with her byline. Her creative energy is fueled by many things: the quiet right before the rest of the world wakes up, the orange sky as the sun rises during an uncrowded morning surf, the beautiful bitter taste of black coffee, and the threatening reminder of a pending deadline.

Subscribe our Newsletter

Get our weekly tips and travel news!

Recommended Articles

10 Filipino Movies That Will Inspire You to Travel the Philippines First I Decided to Become a Digital Nomad in the Philippines & Here’s What I Learned I brought my family along to a 22-day journey around Eastern Mindanao, working online along the way, and here’s what I learned.

LTFRB Suspends Uber: How Is It Affecting Our Travels? So what do the riding public and travellers have to say with Uber’s recent suspension?

Kickstart Your Travel Blogger Status With These 5 Blogging Platforms Are you an aspiring travel blogger? Let this guide help you choose the blogging platform for you!

8 Travel Movies to Watch If You’re Spending the Holidays at Home These ought to give you more travel inspiration.

Latest Articles

Europe Heat Wave 2026: Countries And Cities Most Affected By Record Breaking Temperatures Travel alerts and updates

UAE Visa On Arrival For Filipinos: Eligible Travellers Can Now Enjoy Easier Entry To Dubai And Abu Dhabi Easier UAE travel

Bioluminescence In The Philippines: Best Places To See Glowing Waters And Fireflies Where glowing waters and fireflies can be seen in the Philippines

Bungee Jump Safety Guide After Brazil Rope Incident Involving Fatal Accident What travellers should know

Young Koreans Are Using Fake Shopping Apps to Cope With Stress, Would You Try It? Virtual stress relief